+91 6002993949

submission@iarconsortium.org

Open Access

ISSN (Print) : 2708-5139

ISSN (Online) : 2708-5147

The advancement of the digital world has been made. Access to knowledge from many platforms substantially benefits the community. In keeping with the effective method of working from home during the Covid-19 pandemic, information media is increasingly becoming a space and medium for making investment decisions, enabling the rise and development of investor financial behavior bias. The purpose of this research is to advance behavioral economics, specifically behavioral biases in capital market investment decisions using the echo chamber perspective as a social media representation. The data used is those of online capital market investors with social media or investor community groups. PLS-SEM is used to analyze data (Partial Least Square-Structrural Equation Modeling). Overconfidence, familiarity effect, and irrational exuberance all have a substantial effect on investment decisions in the Indonesian capital market, however gambler's fallacy, financial cognitive dissonance, and echo chamber have no significant effect.

The development of the digital world has made it very easy for people to access information from several platforms. Social media, which was originally a communication medium, has developed into an information medium that provides various information, both what users want or what they don't want, especially when working from home today as an effective way of doing activities during the Covid-19 pandemic. With the increasing accessibility of mobile internet through Smartphone devices, social networking sites such as Facebook, Twitter, Instagram are becoming increasingly important in communicating. While not comparable to traditional one-way mass communication channels such as TV, radio or newspapers, the reach of social media continues to increase, including in low- and middle-income countries.

According to data from Hootsuite, a social media management platform, which released its research at the end of January 2020 in Global Digital Reports 2020, nearly 64 percent of Indonesia's population, or around 175.4 million people, is connected to the internet network, compared to Indonesia's population of around 272, 1 million. When compared to 2019, this figure climbed by 17%, or 25 million users. The average internet user in Indonesia is between the ages of 16 and 64, with a daily usage time of 7 hours and 59 minutes. This condition is higher than the global average of 6 hours 43 minutes each day. According to the same study, the number of social media users in Indonesia has reached 160 million, a rise of 8.1 percent or 12 million users from 2019, As a result, social media usage has reached 59 percent of the overall population in Indonesia. The study's unusual finding is that the average number of accounts owned by Indonesians is ten, with both active and inactive accounts. With 65 percent of Indonesian social media users using it for work.

According to data issued by the Indonesian Central Securities Depository (KSEI), the overall number of capital market investors in Indonesia as of 27 December 2019 was 2.47 million. This figure has climbed dramatically from 1.61 million for the entire year of 2018. According to data issued by the Indonesian Central Securities Depository (KSEI), the overall number of capital market investors in Indonesia as of 27 December 2019 was 2.47 million. This figure has climbed dramatically from 1.61 million for the entire year of 2018 [1]. Space and distance are become irrelevant by the internet. Individuals can readily connect via social media. One of them is social media, which serves as a platform for individuals to share, exchange ideas, and information. As time passes, social media expands and enriches information. Social media is not only a means of social connection with other users, but it is also a source of information from stock businesses. Stock businesses are beginning to investigate this platform since it allows them to reach out to individuals more intimately. Individuals can also communicate with stock firm representatives directly through the same portal. Investors look for faster and more personalized information.

The use of media as a conduit for knowledge is a two-edged sword. The information provided can either assist its users (investors) by generating profits or harm them by bringing losses. Information might elicit differing responses from a group or individual investor, resulting in investor conflicts. Investor disagreements have long been regarded as significant in financial market trading. Indeed, it is difficult to see why investors would trade if there were no source of disagreement [2,3]. Several research have found a correlation between investor disagreement and trading volume and stock performance [4,5,6,7]. Nonetheless, why would investors disagree in the first place, despite the overwhelming evidence of the repercussions of investor disagreement? Leading theory recognizes two major sources of disagreement: disparities in information sets and differences in the models used by investors to understand data [8].

First, disagreements are caused by investor differences of opinion, which can be difficult to discern. Even if a researcher has access to individual-level trading data, which is difficult to obtain, it is difficult to link investors' beliefs to their trades since investors may trade for reasons unrelated to their opinions, such as liquidity. Second, Baron et al. [9] and Rothschild & Sethi, [10] demonstrates that in order to assess whether investor differences in opinion are attributable to disparities in information sets or differences in investor models, researchers should ideally examine investors' trading strategies rather than just actual transactions. Disagreements increase as new information enters the market [11,12]. This is what drives investors to seek information as soon as possible. Investors use a variety of methods to obtain information that is more timely and important than others.

The investor's knowledge is then digested and rationalized or sought to be reasonable in the investor's thinking, resulting in the creation of a space that is consistent with the investor's thinking. Where these rooms have the character that investors seek in order to create an echo chamber. Echo chambers evolved as a result of recent substantial technological advancements in communications and media. The settings and behaviors that enable echo chambers, on the other hand, are not new and have existed for ages. As a result, this study focuses on people's overall tendency to isolate themselves, both offline and online. In fact, the research on the extent of online echo chambers is inconclusive, because internet communication encourages the exchange of diverse viewpoints. Quattrociocchi et al. [13] discovered that there was virtually little communication between the Facebook group and Vicario et al. [14] discovered that conspiracy theories and scientific news result in a homogeneous and divided community of interest groups, Dubois & Blank [15] discovered, on the contrary, that persons with a political interest and diverse media filters preferred to avoid the echo chamber. Furthermore, while the internet is more discrete than offline media, it is far more discrete than face-to-face encounters, as shown Gentzkow & Shapiro [16]. Boxell et al. [17] demonstrates that increased internet use is not always associated with politics. They discovered that the disparities were most pronounced for parents, who were the least likely to use the internet and social media.

To understand echo chambers, we must first understand why people have various chambers. Individuals make numerous decisions that impact which sources of information or influences they experience. These can be major, essential decisions we rarely make, like where to live or what to do with our lives, or tiny decisions we make all the time, like what to read, who to talk to, and what to look for online. Sometimes we make these decisions without considering how they will influence us in the future; for example, if we move to a new place only for the money we can earn there, we may not consider the impact it would have on our future. Similarly, when it comes to investor investment decisions.

The most crucial stage in investment operations is investment decision making. This stage is a decision made by investors to invest in one or more assets in order to increase profits in the future or to pursue another opportunity. This activity is directly tied to involving investor behavior, particularly behavior in dealing with investment risk, in order to identify investors who want risk, are challenged by the existence of risk, or avoid risk. Gender can also have an impact on an individual's investment decisions. Men have a higher level of financial understanding than women, which is especially important when making financial decisions. The level of education also plays a role in risk management; the higher the level of education, the greater the tolerance for risk (risk seeker), because individuals with a high level of education are undoubtedly more financially educated and have an understanding of financial management, including investment. Age also has an impact on investment quality because, as people become older, their risk tolerance increases, but as they reach retirement age, they tend to become risk averse [18].

Several studies have also found that investors' psychology can influence investment decisions or, more specifically, behavioral biases. This is intriguing since behavioral bias can contribute to a country's problem [19] or even if the Covid-19 pandemic conditions have an impact on the capital market [20]. Overconfidence is one example of a behavioral bias related to financial investing. Overconfidence refers to an investor's overwhelming belief in something. Overconfidence leads to overestimation of knowledge and underestimation of predictions made as a result of their superior talents [21]. As a result, this has an impact on investment decisions. Overconfident investors choose high risk with a particular level of return and prefer the kind of investment in real assets, because these assets demand high risk with a maximum rate of return.

The familiarity effect is another interesting behavioral bias to consider because it is related to investors' attitudes toward stock companies. The familiarity effect is frequently defined as an investor's proclivity to buy shares of a well-known stock business or create a portfolio as a result of a selection based on geographical proximity, culture, or even passion for the stock company brand. This circumstance is feasible due to the fact that the information held by investors can differ. When investors understand the risks and returns of an investment, they are more confident and choose the type of investment [22]. Another rationale for the familiarity effect is that investors favor domestic stock companies over overseas ones due to investment obstacles, high transaction costs, and inflation hedges [23] and the familiarity effect occurs in uptrend market conditions [24].

The gambler's fallacy is another behavioral bias that frequently appears in the psychology of investors. The gambler's fallacy is a significant behavioral bias in financial markets. People who are impacted by this tendency misinterpret random sequences. People, in particular, mistakenly identify sequences, leading to the illusion that a specific set of realizations will continue in the future. In financial markets, for example, this bias is visible when investors sell their assets quickly when they are earning and hold on too long when they are losing [25,26,27]. Individuals believe that if something happens in a succession, it will reduce the amount of variation that occurs. This is conceivable in a roulette game, since the probabilities are known with certainty, as opposed to investing in the stock market, where investment options vary and are only restricted by the portfolio constructed.

Another fascinating behavioral bias to investigate is financial cognitive dissonance. This behavior is a manifestation of mental tension, which arises when people have two cognitions or opposing views [28]. When investors experience this situation, they will have an illogical inclination in their thinking when making investment decisions since the thoughts that arise will try to shift values or rationalize actions. The rationalization effort to use the model [29] until it was discovered that age has an effect on cognitive dissonance [30].

Then there was irrational exuberance as the basis of the psychology that gave rise to bubbles in numerous global capital markets. For example, consider the Dutch tulip mania (1634-1637), the Mississippi bubble (1719-1720), and the 1920s stock market boom and crash [31,32], subprime mortgage crisis 2005-2008 [33,34]. The most recent boom cycle in oil prices occurred in 2014. After reaching a high of $100.14 in June, the price of West Texas Intermediate crude oil declined 15% to $53.45 on December 26, 2014, the last trading day of the year. The price then fell to $38, 22 on August 28, 2015, the lowest level in a year. In 2015, the economy began to suffer as a result of these low pricing. US oil businesses, in particular, lay off people in the oil industry. Then, in 2015, a large number of parties began to default on junk bonds.

Irrational exuberance refers to excessive excitement that causes people to think irrationally, as well as the development of behavior to mimic others by justifying price rises in order to elicit excessive enthusiasm [35]. Irrational exuberance is unjustified market excitement that is based on psychological causes rather than fundamental considerations. The role of information becomes very significant in the world of finance; the judgments made by investors will be based on the information collected. Investors will tend to follow one another. Investors flock to any asset that rises in value. They inflate asset prices. Profits become so important to them that they ignore deteriorating economic realities. They participate in a bidding war, driving up prices. As a result, people are investing more money in ventures with continuously falling returns. It may even appear like the price is increasing for a reasonable reason. However, anything can burst that bubble. As a result, when asset prices return to their true market worth, the greed frenzy transforms into fear. Investors sell at any price, even if it is less than their genuine value. After that, the crisis spread to other asset classes. Economic downturn frequently follows, resulting in a recession. A stock market drop frequently triggers a recession due to irrational enthusiasm. This is why it is critical to incorporate irrational exuberance in this study in order to identify future bubbles based on investor behavior in the capital market.

According to the existing description, the purpose of this study is to develop behavioral finance, specifically behavioral bias with a social media strategy in connecting with other investors. With the goal of expanding knowledge and understanding of investors' financial behavior in investment decisions, as well as offering feedback to securities business managers in marketing securities related to investor behavior bias in the capital market.

Behavioral Finance Theory

Behavioral finance theory by Selden [36] based on classical and neoclassical economic theory where behavioral finance (behavioral finance) is a study that has the aim of understanding investor behavior in making investment decisions. Investor behavior in making investment decisions is influenced by investor responses to the opportunities and challenges offered by the ever-changing economic environment [37]. Behavioral finance seeks to clarify and improve understanding of investors' reasoning patterns, including the emotional processes involved and the extent to which they influence the decision-making process. Behavioral finance tries to explain the what, why, and how of finance and investing, from a human perspective [38,39,40]. For example, behavioral finance studies financial markets and provides explanations for many stock market anomalies (such as the January effect), speculative market bubbles (the recent Internet retail stock frenzy of 1999), and crashes (the crashes of 1929 and 1987).

Prospect Theory

Prospect theory is a theory that explains how a person makes decisions in uncertainty. The substance of this theory is in the process of making individual decisions as opposed to the formation of prices that occur. This prospect theory originated from research conducted by Kahneman & Tversky [41] about human behavior that is considered strange and contradictory in making a decision. This theory argues that there is a persistent bias motivated by psychological factors that influence people's choices under conditions of uncertainty. Prospect theory considers preferences as a function of "decision weights," and assumes that these weights do not always match probabilities. In particular, prospect theory suggests that decision weights tend to be over low probability and under medium and high probability weights. Schwartz [42] articulates that "subjects (investors) tend to evaluate prospects or possible outcomes in terms of gains and losses relative to some reference point rather than the final state of wealth."

This study employs a quantitative method to data processing and testing in order to obtain a clear picture of the phenomena that occur, and a comprehensive conclusion is drawn in accordance with the relevant theory. This study employs primary data gathered directly using electronic questionnaire media via network media in the capital market investor group, with the non-probability sampling strategy applied. Respondents with a minimum age of 18 who utilize social media accounts, investor community groups, and company websites come from the Indonesian islands of Java, Bali, Kalimantan, and Sumatra. A 5-point Likert scale was used to collect measurements for the model's primary dependent and independent variables. Data analysis in this study used descriptive analysis and statistical analysis through the outer model and inner model in PLS-SEM. PLS-SEM is designed to overcome problems in multiple regression. Technically, the goal is to create a model that transforms a set of associated explanatory variables into a new set of variables that are not mutually linked. PLS-SEM analysis is divided into two stages: the outside model and the inner model. The outer model can be used to examine the validity and reliability of the indicators on the latent variables, while the inner model can be used to examine the influence of latent variables on one another.

In this study, the outer model is separated into two parts: explanatory factor analyses and confirmatory factor analyses. Explanatory factor analysis (EFA) is used in indicators that measure the latent variable in a formative manner, whereas confirmatory factor analysis (CFA) is used in indicators that measure the latent variable in a reflective manner. An indicator is said to be valid in confirmatory factor analysis if the loading factor value of the indicator measuring the latent variable is larger than 0.4 and the average variance extracted (AVE) value is greater than 0.5. If the composite reliability (CR) and Cronbach alpha (CA) values are greater than 0.7, the indicator is said to be reliable. In the explanatory factor analysis, the indicator is said to be valid if the loading factor value of the indicator measuring the latent variable is greater than 0.4 with a significance value of 0.05, and the indicator is said to be reliable if the value of composite reliability (CR) and Cronbach alpha is greater than 0.7.

The link between latent variables is described by the inner model. The inner model is split into two parts: hypothesis testing and coefficient of determination. In hypothesis testing, a link between latent variables is said to be significant if the P-value is less than 0.05 or the t-count is greater than 1.96. While the coefficient of determination, there are three criteria, namely, the influence between the latent variables are said to be strong if the value of R2 > 0.67; moderate if 0.33 <R2 ≤ 0.67; weak if the value of 0.19 <R2 ≤ 0.33 and said to be very weak if the value of R2 ≤ 0.19.

The data collection findings yielded 204 investor respondents who are members of securities companies in the Indonesian capital market. After that, the data was processed using the PLS-SEM (Partial Least Squares-Structural Equation Modeling) method. The respondents are described IN Table 1.

According to Table 1, the majority of respondents are male 122 people (59.80%), with an age range of more than 36 years (57.84%), with the most recent education Bachelor 160 people (78.43%), and domiciled or domiciled in East Java (48.04%), which includes Surabaya, Sidoarjo, Mojokerto, Probolinggo, Pamekasan, Trenggalek, Kediri, and Gresik. The majority of those who completed the questionnaire had 3-4 years of capital market investment experience (42.16%).

Table 1: Respondent Description

Demographics | Category | Frequency | Percentage |

Gender | Man | 122 | 59.80% |

Woman | 82 | 40.20% | |

Age | 17 – 26 years old | 4 | 1.96% |

27 – 36 years | 82 | 40.20% | |

Over 36 years | 118 | 57.84% | |

last education | SMA / SMK | 15 | 7.35% |

Diploma | 24 | 11.76% | |

S1 | 160 | 78.43% | |

S2 | 5 | 2.45% | |

Investment Experience | Less than 1 year | 29 | 14.22% |

1-2 years | 54 | 26.47% | |

3-4 years | 86 | 42.16% | |

More than 5 years | 35 | 17.16% | |

Domicile | East Java | 98 | 48.04% |

Central Java | 34 | 16.67% | |

West Java | 10 | 4.90% | |

Jakarta | 33 | 16.18% | |

Depok | 9 | 4.41% | |

Denpasar | 5 | 2.45% | |

Medan | 6 | 2.94% | |

Balikpapan | 5 | 2.45% | |

Makassar | 2 | 0.98% | |

Pekanbaru | 2 | 0.98% | |

Social Media Account | 108 | 52.94% | |

93 | 45.59% | ||

26 | 12.75% | ||

Telegram | 37 | 18.14% | |

IDX | 45 | 22.06% | |

20 | 9.80% | ||

Other | 5 | 2.45% |

Source: Processed questionnaire results

Table 2: Outer Model

Parameters | CR | CA | AVE | Full VIFs | R-squared | Adjusted R-squared |

Overconfidence | 0.927 | 0.907 | 0.745 | 1.440 | 0.610 | 0.598 |

Familiarity Effect | 0.768 | 0.729 | 0.722 | 2.800 | ||

Gambler's Fallacy | 0.839 | 0.740 | 0.773 | 2.672 | ||

Financial Cognitive Dissonance | 0.874 | 0.818 | 0.881 | 2.901 | ||

Irrational Exuberance | 0.805 | 0.733 | 0.790 | 2.294 | ||

Echo Chamber | 0.834 | 0.747 | 0.617 | 1.923 | ||

Investment Decision | 0.790 | 0.782 | 0.789 | 1.800 |

Table 3: Path Analysis and Hypothesis Testing

Path | Coefficients | P-Value | Effect Size | Conclusion |

OverconfidenceàInvestment Decision | 0.544 | <0.001 | 0.345 | Supported |

Familiarity Effectà Investment Decision | 0.193 | <0.001 | 0.094 | Supported |

Gambler's FallacyàInvestment Decision | 0.068 | 0.164 | 0.031 | Not Supported |

Financial Cognitive DissonanceàInvestment Decision | 0.147 | 0.016 | 0.071 | Not Supported |

Irrational ExuberanceàInvestment Decision | 0.236 | <0.001 | 0.106 | Supported |

Echo ChamberàInvestment Decision | -0.089 | 0.099 | 0.036 | Not Supported |

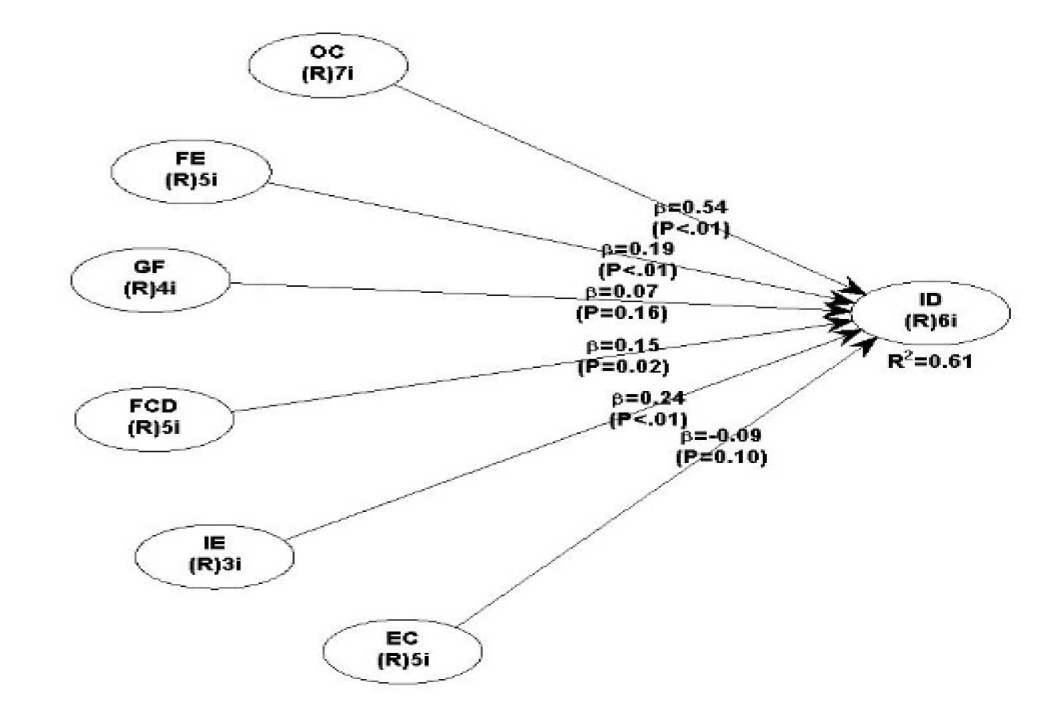

Figure 1: PLS-SEM model

Statistical Results

Several phases of data processing were performed utilizing the Partial Least Squares-Structural Equation Modeling (PLS-SEM) approach. This strategy is thought to be capable of overcoming the problem of multiple regression by building a model that converts a collection of correlated explanatory factors into a new set of uncorrelated variables. The obtained measurement model (outer model) is then evaluated based on the substantive content model, specifically by comparing the relative magnitude of the weight and the significance of the weight, and the inner model is evaluated by looking at the percentage variance, the R-squared value, and the magnitude of the structural path coefficient. The Partial Least Squares-Structural Equation Modeling yielded the following results (PLS-SEM).

According to the results in Figure 1 and Table 2, practically all of the loading factor values of the indicators are greater than 0.7. According to Chinn (1998), an indicator is regarded to have good dependability if its value is larger than 0.7, but a loading factor of 0.5 to 0.6 can still be maintained for models in development, hence these results show that the validity criteria have been met. Table 2 also provides the composite reliability value, and Cronbach's alpha is greater than 0.7, indicating that the reliability standards were met. All indicators, it can be argued, are capable of measuring investment decision variables such as overconfidence, familiarity effect, gambler's fallacy, financial cognitive dissonance, irrational exuberance, and echo chamber.

The structural model evaluation step is the next level of the PLS-SEM study. At this point, the whole collinearity VIF, p-value, R Square, and path coefficients are examined to determine the influence of each variable, either directly or indirectly. According to Table 2, the adjusted R squared value for investment decisions is 0.598, with a R squared value of 0.610 and a p-value of 0.005 (0.001). This model also lacks multicollinearity because the VIF values are all less than 5. The R-squared value is in the range of 0.33 to 0.67, indicating that the variable has a modest influence.

Overconfidence was found to have a substantial effect on investing decisions, with a coefficient of 0.544 and a p-value of 0.001. Based on these findings, implying that overconfidence has a considerable and beneficial effect on investing decisions. As a result, investors' overconfidence can influence capital market investment decisions. This demonstrates that capital market investors have an overabundance of confidence in their investment selections, which can jeopardize their investments if they do not pay attention to the fundamentals of the stock. Overconfidence was found to be a predictor of investment decisions in this study. The findings of this study back up the findings of the study by Armansyah 1 that overconfidence is proven to be a predictor of investment decisions of capital market investors and also supports Nofsinger [21]. This outcome is achievable because confidence is required when making capital market investment decisions because every action involves a risk. This conclusion differs from the research findings by Fachrudin et al. which shows overconfidence has no effect on investment decisions.

The Familiarity Effect had a significant influence on investment decisions, with a coefficient of 0.193 and a p-value of 0.001. According to these studies, the Familiarity Effect has a large and beneficial influence on investment decisions. As a result, the introduction of securities companies by investors can impact capital market investment decisions. This demonstrates that capital market investors tend to incorporate stock companies, securities companies, and even the investment environment into their investment decision-making process. This is understandable because investors need to feel safe and minimize risk in their investments, and when investors feel safe, investments are made. The Familiarity Effect was found to be a predictor of investment decisions in this study. The findings of this investigation back up the findings of the previous study by Djojopranoto & Mahadwartha [24] that the Familiarity Effect is proven to be a predictor of investment decisions of capital market investors and also supports Nofsinger [21] where investors tend to feel safe if they invest their funds in companies that have been known or products that have been known before. According to a statement made by Ackert & Deaves; Kumar & Goyal [23], it is also clear that investors prefer to invest in domestic markets rather than global markets due to regulatory variations across countries as well as inflation hedging difficulties.

With a coefficient of 0.068 and a p-value of 0.164 (>0.001), the influence of gambler's fallacy on investing decisions was shown to be minor. According to these findings, there is no significant effect of the gambler's fallacy on investment decisions. As a result, investors' perception that if something happens twice in a succession, it will happen again cannot affect capital market investment decisions. This demonstrates that capital market investors do not expect a repeat of a desired capital market condition in the investment decision-making process, which is understandable given investors' strong confidence in investing and caution in making decisions. The gambler's fallacy was not demonstrated to be a predictor of investing decisions in this study. The results of this study support the results of the study Fachrudin et al. that the gambler's fallacy is proven not to be a predictor of investment decisions by capital market investors where investors tend to be careful and have high confidence when investing their funds. The results of this study are different from the results of Djojopranoto & Mahadwartha [24] who found that the gambler's fallacy occurs during uptrend conditions, as well as research from Suetens & Tyran against Danish men and young age or college level who tend to do the gambler's fallacy.

With a coefficient of 0.147 and a p-value of 0.016 (>0.001), the influence of Financial Cognitive Dissonance on investment decisions was determined to be insignificant. According to these data, there is no significant influence of Financial Cognitive Dissonance on investing decisions. As a result, the mental strain experienced by investors on the two cognitions cannot influence capital market investment decision making. This demonstrates that capital market investors tend to ignore or control the tensions experienced during the investment decision-making process. This is quite reasonable because investors have media sharing both from securities companies, between investors, and information from stock companies, so tensions that occur are more easily muted or even controlled. Financial Cognitive Dissonance was not found to be a predictor of investing decisions in this study. The results of this study support the results of the study Pradhana that Financial Cognitive Dissonance is proven not to be a predictor of investment decisions of capital market investors where investors tend to have cognitive control on investment decision making. The findings of this study differ from those of Afreen Fatima; Kanojia et al. [30], who discovered that Financial Cognitive Dissonance occurs in different age groups, sacrificing rationality; this is possible due to regional demographic differences as well as technological and communication developments, resulting in differences in information dissemination.

With a coefficient of 0.236 and a p-value of 0.001, the influence of irrational exuberance on investment decisions was determined to be significant. Based on these findings, it appears that irrational exuberance has a significant impact on investment decisions. As a result, investor enthusiasm that leads to speculation might impact investment decisions in the capital market. This demonstrates that the enthusiasm of capital market investors occurs in the investment decision-making process; conditions like this can endanger the capital market because investors who are triggered by the euphoria of market trends will bring up psychology that is not based on the foundation of fundamentals, causing them to invest in speculation. Investment conditions that follow a pattern like this can lead to the emergence of a bubble or speculative bubbles that can grow in size before bursting and causing a market crash. The rapid growth of communication media also supports the occurrence of irrational exuberance, because there are many opinions or inputs in a communication space that become a source of information for investors. In this study irrational exuberance proved to be a predictor of investment decisions. The results of this study support the results of research by Ackert et al. that irrational exuberance is part of the investment decisions of capital market investors where price increases trigger investor enthusiasm in making investment decisions. This psychological condition of investors is possible because it is in accordance with prospect theory that there is a continuous bias motivated by psychological factors that influence investment decision making choices.

With a coefficient of -0.089 and a p-value of 0.099 (>0.001), the influence of echo chamber on investment decisions was found to be insignificant. According to these findings, there is no significant effect of the echo chamber on investment decisions. As a result, investors' trust in the information gained in their echo chamber cannot impact capital market investment decisions. This demonstrates that investors use social media as a means of communication and a source of information in the investment decision-making process, which is understandable given that investors have a high level of confidence in their investments and are cautious when making judgments. The echo chamber was not demonstrated to be a predictor of investing decisions in this study. The results of this study are in line with research Cardenal et al. where investors use social media and media provided by the exchange as part of the decision-making process, but in this study the echo chamber cannot be used as a predictor of investment decisions.

Overconfidence, familiarity effect, gambler's fallacy, financial cognitive dissonance, irrational exuberance, and echo chamber were found to have a significant effect on investing decisions, with an R-squared value of 0.610 (Table 2 and Figure 1) and p-value 0.001. Based on these findings, hypothesis 7 is accepted, implying that overconfidence, familiarity effect, gambler's fallacy, financial cognitive dissonance, irrational exuberance, and echo chamber have a significant and positive effect on investment decisions.

Based on the findings of the research, it is possible to conclude that the variables overconfidence, familiarity effect, and irrational exuberance all have a substantial impact on investment decisions in the Indonesian capital market. The concept of echo chamber perspective was then applied in this study, which discovered that investors in the respondents tend to use social media and information media provided by the stock exchange and securities as a medium for sharing information and receiving recommendations in analyzing the capital market before choosing stocks in order to provide convenience in the decision-making process. This is possible because the poll was administered through social media intermediaries to capital market investors, thus investor respondents had social media that they use to engage with other investors. These findings on irrational exuberance and echo chambers add to current theoretical contributions and demonstrate that irrational exuberance influences investment decisions in the Indonesian capital market, thus enhancing the theory of capital market investor behavior.

The study's findings may have technical implications for practitioners, particularly providers of communication media between investors. The findings indicate that investors pay attention to the development of stock firms via information media provided by securities companies and social media owned by investors, as well as input gained from other investors in supporting analysis in the decision-making process. Regarding this condition, developers of investor communication media can see it as an opportunity to provide good service through information on market condition analysis and stock company introduction in order to attract more investors' interest in capital market investment while also detecting capital market bubbles that may occur, though this still requires more in-depth research.

Suggestions that can be conveyed in accordance with the development of this research are that in future research, other research can develop investment behavior models by including more financial behavior and financial behavior deviations because these factors, in addition to personality traits or the big five approach, are still considered to be the main trigger of market behavior. Personality traits and ocean models can also be used to develop this research so that it can produce different or similar outcomes to the results of this study for future scientific breakthroughs.

There are various limitations to this study. First, data was gathered from respondents who completed electronic surveys issued via forums, groups, and emails in the hopes of contacting respondents who met the necessary criteria. As a result, this study may not reflect all Indonesian capital market investors. Data for future research can be gathered from a variety of sources, including system user discussion forums and cross-cultural studies. Second, this study focuses on the advantages of employing technology, particularly social media, by including an echo chamber as a media component in which investors' financial activity has its own area to transmit and get support for ideas. More sophisticated models that can explain more elements connected to behavioral finance can be developed in future research. Other ways are also suggested in an effort to advance this research in order to achieve more up-to-date research that can overcome the current restrictions.

Armansyah, R. F. “A Study of Investor Financial Behavior on Online Trading System in Indonesian Stock Exchange: E-Satisfaction, E-Loyalty, and E-Trust.” Journal of Economics, Business, & Accountancy Ventura, 2020.

Karpoff, Jonathan M. “A Theory of Trading Volume.” The Journal of Finance, 1986.

Milgrom, Paul, and Nancy Stokey. “Information, Trade and Common Knowledge.” Journal of Economic Theory, 1982.

Atiase, R. K., et al. “The Fundamental Determinants of Trading Volume Reaction to Financial Information.” Journal of Financial Research, vol. 34, no. 1, 2011, pp. 61–101.

Banerjee, Snehal, and Ilan Kremer. “Disagreement and Learning: Dynamic Patterns of Trade.” The Journal of Finance, 2010.

Diether, Karl B., et al. “Differences of Opinion and the Cross Section of Stock Returns.” The Journal of Finance, 2002.

Jung, H., and S. Moon. “Matching Level and Investors’ Heterogeneous Beliefs.” Journal of Applied Business Research, 2017.

Hong, Harrison, and Jeremy C. Stein. “Disagreement and the Stock Market.” Journal of Economic Perspectives, 2007.

Baron, Matthew, et al. “Risk and Return in High-Frequency Trading.” Journal of Financial and Quantitative Analysis, 2019.

Rothschild, David, and Rajiv Sethi. “Trading Strategies and Market Microstructure: Evidence from a Prediction Market.” Journal of Prediction Markets, 2016.

Banerjee, Snehal, et al. “When Transparency Improves, Must Prices Reflect Fundamentals Better?” Review of Financial Studies, 2018.

Kondor, Péter. “The More We Know about the Fundamental, the Less We Agree on the Price.” Review of Economic Studies, 2012.

Quattrociocchi, Walter, et al. “Echo Chambers on Facebook.” SSRN Electronic Journal, 2018.

Del Vicario, Michela, et al. “The Spreading of Misinformation Online.” Proceedings of the National Academy of Sciences, 2016.

Dubois, Elizabeth, and Grant Blank. “The Echo Chamber Is Overstated.” Information, Communication & Society, 2018.

Gentzkow, Matthew, and Jesse M. Shapiro. “Ideological Segregation Online and Offline.” Quarterly Journal of Economics, 2011.

Boxell, Levi, et al. “Greater Internet Use Is Not Associated with Faster Growth in Political Polarization.” Proceedings of the National Academy of Sciences, 2017.

Lutfi, Lutfi. “The Relationship Between Demographic Factors and Investment Decision in Surabaya.” Journal of Economics, Business, & Accountancy Ventura, 2011.

Armansyah, R. F. “Herd Behavior and Indonesian Financial Crisis.” Journal of Advanced Management Science, 2018.

Allam, S., et al. “Determinants of Herding Behavior in the Time of COVID-19.” SSRN Electronic Journal, 2020.

Nofsinger, John R. The Psychology of Investing. Routledge, 2016.

Lestari, W., and R. Iramani. “Persepsi Risiko dan Kecenderungan Risiko Investor Individu.” Jurnal Keuangan dan Perbankan, 2013.

Kumar, S., and N. Goyal. “Behavioural Biases in Investment Decision Making.” Qualitative Research in Financial Markets, 2015.

Djojopranoto, R. R., and P. A. Mahadwartha. “Pengujian Bias Perilaku.” Jurnal Akuntansi dan Keuangan Indonesia, 2016.

Armansyah, R. F. “The Disposition Effects on the Financial Crisis of the Indonesian Capital Market.” Jurnal Manajemen dan Kewirausahaan, 2018.

Barber, Brad M., and Terrance Odean. “The Behavior of Individual Investors.” Handbook of the Economics of Finance, 2013.

Chen, G., et al. “Trading Performance, Disposition Effect, Overconfidence, Representativeness Bias, and Experience.” Journal of Behavioral Decision Making, 2007.

Olsen, Robert A. “Cognitive Dissonance.” Journal of Behavioral Finance, 2008.

Beunza, Daniel, and David Stark. “From Dissonance to Resonance.” Economy and Society, 2012.

Kanojia, S., et al. “Factors Influencing Individual Investors in the Indian Stock Market.” IOSR Journal of Business and Management, 2018.

Garber, Peter M. Famous First Bubbles. MIT Press, 2018.

White, Eugene N. “The Stock Market Boom and Crash of 1929 Revisited.” Journal of Economic Perspectives, 1990.

Adelino, Manuel, Antoinette Schoar, and Felipe Severino. “Loan Originations and Defaults in the Mortgage Crisis.” Review of Financial Studies, 2016.

Rosefielde, Steven, and Daniel Q. Mills. “Subprime Mortgage Crisis.” Democracy and Its Elected Enemies, 2013.

Shiller, Robert J. Irrational Exuberance. 3rd ed., Princeton University Press, 2015.

Selden, G. C. Psychology of the Stock Market. 1912.

Puspitaningtyas, Zarah. “Perilaku Investor dalam Pengambilan Keputusan Investasi di Pasar Modal.” Jurnal Akuntansi Universitas Jember, 2013.

Ricciardi, Victor, and Helen K. Simon. “What Is Behavioral Finance?” Business, Education and Technology Journal, 2000.

Statman, Meir. “What Is Behavioral Finance?” Handbook of Finance, 2008.

Zaleskiewicz, Tomasz. “Behavioral Finance.” Handbook of Contemporary Behavioral Economics, 2015.

Kahneman, Daniel, and Amos Tversky. “Prospect Theory: An Analysis of Decision under Risk.” Econometrica, 1979.

Schwartz, Howard. “Behavioural Economics and Entrepreneurial Decision Making.” Global Business and Economics Review, 2007.