+91 6002993949

submission@iarconsortium.org

Open Access

ISSN (Print) : 2708-5139

ISSN (Online) : 2708-5147

Inventories are essential assets of a company's production process. In order to prevent losses resulting from stock deficits and surpluses, control of such inventories is useful. The aim of this paper is to analyse the effect on financial performance of inventory management measured in terms of inventory conversion time and inventory turnover measured in terms of return on assets, cash flow from operations and market value added of listed manufacturing companies in Sri Lanka. A conceptual framework is designed to represent direct and indirect relationships among these constructs. This study adopted a quantitative research approach. Secondary data was collected for a period from 2014 to 2018 using published annual reports of Listed manufacturing Companies in the Colombo Stock Exchange, Sri Lanka. The sample size included 29 manufacturing companies and the sample was selected through the judgmental sampling technique. Results of this study show that inventory conversion period has a significant negative relationship on return on assets, cash flow from operations and market value added of a firm. Thus, lower the time taken to convert inventories to sales, higher the financial performance vice versa. However, the results indicate that inventory turnover is insignificantly related to financial performance of manufacturing companies in Sri Lanka. It is expected that the model further improves the knowledge on understanding the importance of inventory management on financial performance of a company. It could be valuable to the managers of a company to identify their role in managing inventories.

Inventory management comprises of various techniques used to determine the right quantity of an inventory item at the right time and place [1]. Inventories are current assets that form a significant part of the assets of a firm which has a resale value that earn profit to the respective firm. Thus, better management of those inventories will release capital productively [2]. Inventory management provides the possibility to meet the reported demand at an appropriate level and to avoid surplus of production and deficit by careful inventory monitoring and forecasting [3].

Inventory costs mainly includes costs such as warehousing, loading, transportation, insurance, inventory losses, loss of volume discounts, stock outs and capital costs [3]. Thus, Inventory represent the largest costs to manufacturing and trading, retail and wholesale firms as inventory represents approximately of 20%- 30% of their total investments [2]. Therefore, there is a significant task to an inventory manager to decide the right quantity of inventory to keep and estimate the appropriate time to reorder those inventories to eliminate issues such as losses and stock outs of inventories.

According to Karim et al. [4] failure to manage inventories may affect the financial performance as it leads to a significant increase in amount of losses. Financial performance refers to how effectively a firm is using its resources to generate sales using their essential enterprise methods subjectively Anshur et al. [5]. Recent evidences prove that failure to manage inventory has almost caused the demise of some companies. “Ralph Lauren’s iconic clothing” an American sportswear company in which profits were plummeted by 50 percent in the two years of 2014, 2015 solely for the reason that they couldn’t get their inventory under control. Furthermore, companies like Kmart, Nike, best buy, Walmart also have faced the same consequences [6].

Performance of a firm and its managers are directly impacted by the effectiveness of an inventory management system [7]. Therefore manager’s objectives should not always solely consider to satisfy customer’s expectations. It is important that the managers of a firm to satisfy customer needs while maintaining inventory at a minimum cost [8]. Moreover Karim et al. [4] suggests that there should be further investigation to determine the root cause of the problem that failure to manage inventories impact on financial performance. Thus, this study aims to verify the cause-and-effect relationship between effective inventory management and the financial performance of a listed manufacturing firm.

Inventory management is an evolutionary concept that every organization deals with from the beginning to the demise of their lifecycle. According to Stanger et al. [9] inventory performance of a firm can be increased by using six practical lessons which are recruiting experienced staff, understanding target stock levels and patterns of orders, monitoring remaining shelf life, transparency of inventory and keeping procedures simples as possible. The study further states that management of perishable inventory leads to success of an organization. By having an optimum inventory investment, a company can increase their rate of return and minimize the risk of liquidity and loss of business [10]. Implications of successful inventory management include minimization of inventory and costs while improving profitability.

Inventory management of a company depends on the nature of the company and the country in which it operates. In the examination of inventory behaviour and its effect on financial performance of OECD countries, Roumiantsev and Netessine [11] found that there is a 76% to 95% variation of absolute inventory depending on the country.

Study revealed that inventory management measured in terms of inventory turnover is weakly related to the overall company performance. The study concludes that inventory management itself cannot be a factor to increase performance. In contradiction to that Leachman et al. [12] in their study concluded that variations in manufacturing performance is subsequently explained by variation in inventory turnover.

Furthermore, Shah and Shin [13] findings state that reductions in the level of inventories are positively related to the financial performance of a firm. Further the researcher states that higher inventory turnover, lower inventory to sales ratio and lower the days taken to convert inventory to sales has positive effects of financial performance of a firm. However, Roumiantsev and Netessine [11] states that inventory turnover is related to organizational performance and has a negative relationship with firm’s performance.

Further contradiction is presented by Mathuva [14] which states that firms should keep higher inventory levels to increase performance as it avoids costs of possible interruptions and possible loss of business due to scarcity. Accordingly, Augustine and Agu [15] management of an organization should monitor and manipulate inventory systems to maintain the consistency in their production to increase profitability and effectiveness. In addition to that, Shin et al. [16] reveals that efficient inventory management practices have a positive effect on the profitability of a firm in US manufacturing firms.

Folinas and Shen [17] concluded that variable inventory turnover doesn’t relate to the financial performance of a company and inventory conversion days play a role in the relationship up to a certain degree. On the contrary, Shardeo [2] reveals that there is an impact of inventory management on the financial performance of a company and inventory turnover ratio used to measure inventory management is related to the net profits of steel manufacturing companies of India. In addition, Altan and Sekeroglu [18] states that inventory turnover ratio shows the success of a business in its management of inventory. However, the study further explains that industry specific and economic conditions of the host country can vary the resulting profitability from inventory policies.

According to Sunday and Joseph [19], there is a positive relationship between inventory turnover ratio and the profitability of a firm while there is a negative relationship between inventory conversion period and the profitability of a firm. In contrast to the above finding Karim et al. [4] reveals that poor inventory management has a modest influence to the financial performance of a firm and financial ratios are not heavily influenced by poor inventory management.

This study attempts to investigate the relationship between inventory management and the financial performance of listed manufacturing firms in Sri Lanka in both accounting based and broader market-based perspective.

Data gathered from all 38 manufacturing firms listed in the Colombo Stock Exchange. Total number of observations lies in between 190-200 received for the period of 2014-2018. The general-purpose statistical software package (STATA) is used to analyse the following panel regression models.

Model 1

Model 2

Model 3

Measures of variable are discuss in Table 1.

Table 1: Measures of variables

Variables | Indicators | Measurement |

Independent Variables | ||

Inventory Conversion Period | How fast Inventories are converted into Sales |  |

Inventory turnover | How many times inventory is turned into sales in a year |  |

Dependent Variable | ||

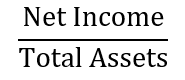

Return on Assets | How much return generated from assets of a firm |  |

Market Value Added | Return generated extra from the money invested |

|

Cash Flow from Operations | Cash generated from core activities of a firm |  |

Control Variables | ||

Operating Efficiency | Reduction in operating expenses compared to sales |  |

Firm growth | Sales growth of a firm |  |

Firm Size | The number of Total assets in a firm |  |

Table 2: Descriptive statistics

Variable | Mean | Std. Deviation | Min | Max | N |

ROA | 0.072 | 0.114 | -0.292 | 0.494 | 145 |

CFO | 0.034 | 0.308 | -2.165 | 0.775 | 145 |

MVA | 8.778M | 0.699 | 6.975M | 10.631M | 145 |

ICP | 131.547 | 197.387 | 4.226 | 1621.594 | 145 |

IT | 6.407 | 9.372 | 0.225 | 86.377 | 145 |

OE | 10.102 | 101.809 | -26.084 | 1225.186 | 145 |

FG | 0.239 | 1.496 | -0.583 | 17.684 | 145 |

FS | 9.334M | 0.484 | 8.315M | 10.447M | 145 |

M: Millions

Table 3: Test for Multicollinearity

Variables | ICP | IT | OE | FG | FS |

ICP | 1.0000 |

|

|

|

|

IT | -0.2601 | 1.0000 |

|

|

|

OE | -0.0206 | -0.0395 | 1.0000 |

|

|

FG | -0.0470 | 0.0948 | -0.0192 | 1.0000 |

|

FS | -0.1699 | -0.2004 | -0.1073 | -0.0376 | 1.0000 |

Analysis

The focus of this section is on the findings and the discussion of the results compared with the literature. The paper presents conclusions on the effect of inventory management on financial performance of listed manufacturing companies in Sri Lanka.

Descriptive Statistics

According to the Table 2 descriptive Summary, the average value of Return on Assets (ROA) of listed manufacturing firm in Sri Lanka is 7.2%. This indicates that assets of a firm generate only 7% of the profits, which is relatively low. The average value of cash flow from Operations (CFO) of a firm is 3.4%. This indicates that the cash flow generated from operating activities of a firm is only 3.4% of sales of that company. The results also indicate that the average Market value Added of a firm is 8.778.

Furthermore, the results indicate that the average Inventory conversion period for a listed manufacturing firm in Sri Lanka is 131.5 days. In addition to that the results indicate the average inventory turnover of a firm is 6.4 times which indicates that inventory is turned into sales at an average of 6.4 times a year. Apart from that, the control variables used in the study which are Operating efficiency, Firms growth and Firm size has average values of 10.1, 0.24, and 9.33 respectively.

Multicollinearity

Correlation analysis was performed to determine whether there a correlation between the independent variables used in the study. The correlation analysis explains the direction and strength of the relationship between two variables.

According to the Table 3, the conclusion is that there are weak correlations between all the variables. This is because the correlation between the variables is lesser than 0.6. Thus, there is a very low or no multicollinearity.

Random Effect or Fixed Effect

The existence of a random effect or fixed effect was evaluated in both models. First, models were tested to identify whether there are fixed effects in the model. F test was used to identify the best method among pooled OLS and Fixed effect method. The result of the model 01 show that Prob > F = 0.1773. Therefore, pooled OLS method was preferred for model 01. The result of the model 02 show that Prob > F = 0.0092. Therefore, null hypothesis is rejected which concludes that there are fixed effects in the model. The result of the model 03 show that Prob > F = 0.1307. the p-value of the F-test is higher than 0.05, therefore null hypothesis is accepted and concludes that there are no fixed effects. Therefore, pooled OLS method was preferred.

Next, the Breusch and Pagan Lagrangian multiplier test was used to determine the best method among pooled OLS method and Random effect method. The results of the model 01 show that Prob > chibar2 = 0.0000. Thus it concludes that the Random effect model is preferred for model 01. Similarly, The results of the model 02 show that Prob > chibar2 = 0.1379. Thus it concludes that there are no random effects in the model. Thus the model 02 was intiated through Fixed effects method. The results of the model 03 show that Prob > chibar2 = 0.0000. the p-value of the test is lower than 0.05 therefore null hypothesis is rejected. Thus, it concludes that there are random effects and the Random effect model is preferred for this model.

Autocorrelation, Heteroskedasticity, Cross Sectional Dependence

The test of serial correlation (autocorrelation) was performed using the Wooldridge test for autocorrelation. If P value is higher than 0.05, it indicates that there is no autocorrelation in this model. The results for model 01 indicate that Prob > F = 0.1615. For model 02 it indicates that Prob > F = 0.7360. The result of model 03 shows that Prob > F = 0.1307. Thus there areno autocorrelation in all three models.

Also, to determine whether there is heteroskedasticity in the model the wald test was ran. The null hypothesis is rejected if the p-value is lower than 0.05 and concludes the availability of heteroskedastocity. The results of all three models at Wald test is Prob > chibar2 = 0.0000. Therefore, it concludes that all the models have heteroskedasticity.

Afterwards the pesarans’s test of cross sectional dependence was performed for all the models. Null hypothesis states that there is no cross sectional dependance. The results for model 01 and model 02 indicate a Pr = 0.000. Therefore null hypothesis is rejected and conclude that there is cross sectional dependance in the model. The results for model 03 indicate a Pr = 0.5131. Therefore null hypothesis is accepted and conclude there is no cross sectional dependence in the model.

Thus the final result for model 01 and model 03 were derived using cluster option to correct the issue of autocorrelation in the random effect model. For model 02 final results was derived by using cluster option to correct the issue of Heteroskedasticiy and Cross sectional dependance in the fixed effect model (Table 4).

Results from the three models provide that inventory conversion period is negatively related to return on assets, cash flow from operations and market value added of a firm. Thus, one finding of the study is that inventory conversion period of a firm is negatively related to financial performance. This indicates that when more time is taken to convert inventories, financial performance of a firm would decline. The results also indicate that inventory conversion period is significantly related to financial performance. These findings are consistent with the findings of Sunday and Joseph [19] and Sitienei and Memba [20] and is inconsistent with the findings of Mathuva [14].

The results derived from the variable inventory turnover is that there is a positive impact from inventory turnover to cash flow from operations of a firm and has a negative impact to return on assets and market value added of a firm. However, the results from all three models are Insignificant. The finding is that inventory turnover is insignificantly related to financial performance of a firm. These findings are consistent with the findings of Folinas and Shen [17].

Control variables of the model one present mixed result to return on assets of a firm. Operating efficiency has a negative impact on return on assets of a firm. In addition, firm’s growth has positive relationship with return on assets of a firm. However, firm’s size has a significant positive impact to return on assets of a firm. This indicates that larger the firm size larger the return generated from assets.

Results of control variables in the second model also provide mixed results. Operating efficiency has a positive impact to the cash flow from operations of a firm. Firm’s growth also has a positive impact to cash flow from operations of a firm. Firm’s size has a significant positive impact to cash flow from operations of a firm. This indicates that larger the firm’s size higher the cash flow generated from operations.

Results of control variables form the third model indicates that operating efficiency has a significant positive impact to market value added of a firm. Therefore, higher the operating efficiency of a firm market value addition of a firm increases.

Table 4: Coefficient estimates

| Dependant Variable: ROA(Model 01) | Dependant Variable: CFO(Model 02) | Dependant Variable: MVA(Model 03) | ||||||

Independent variables | Estimates (1) | Standard errors (2) | z-values (3) | Estimates (1) | St. errors (2) | z-values (3) | Estimates (1) | Standard errors (2) | z-values (3) |

ICP | -0.000208*** | 0.0001 | -3.7 | -0.00096*** | 0.0003 | -2.88 | -0.000402*** | 0.0001 | -3.82 |

IT | -0.00071 | 0.0009 | 0.78 | 0.000021 | 0.0024 | 0.01 | -0.000553 | 0.0024 | -0.23 |

OE | -0.00004 | 0.0001 | 0.54 | 0.000041 | 0.0001 | 0.39 | 0.000225*** | 0.0000 | 8.13 |

FG | 0.004068 | 0.0049 | 0.83 | 0.001594 | 0.0060 | 0.26 | 0.006867 | 0.0064 | 1.07 |

FS | 0.056973*** | 0.0092 | 6.17 | 0.149207*** | 0.0401 | 3.72 | 0.875917*** | 0.1549 | 5.65 |

Cons | -0.42415 | 0.0879 | -4.83 | -1.233473 | 0.3609 | -3.42 | 0.654686 | 1.4570 | 0.45 |

No.of groups | 29 |

|

| 29 |

|

| 29 |

|

|

No. of observations | 145 | 145 | 145 | ||||||

p-value | 0 | 0.0049 | 0 | ||||||

R-squared | 0.222 |

|

| 0.4837 |

|

| 0.3788 |

|

|

This table reports coefficients, standard errors and z-values from the estimation of Equation ROA in Columns (1), (2) and (3) respectively. *,**,***Denote statistical significance at the 10%, 5% and 1% level, respectively

The results also show that firm’s size has a significant positive impact to market value added of a firm. Therefore, larger the firm higher the market value addition. Therefore, in overall, it is observed that firm’s size has a positive significant impact on financial performance. This is consistent with the findings of Sitienei and Memba [20] and Gaur and Kesavan [21].

In overall, the main findings of this study are that inventory conversion period has a significant negative impact to financial performance of a firm, inventory turnover is insignificantly related to financial performance of a firm.

Inventory management is an important tool used to enhance productivity and quality of assets of a company. It is a technique used to manage inventories in a way that losses can be avoided. Inventory represents approximately of 20-30% of a total investments of manufacturing business. Therefore, effective inventory management in a manufacturing business is crucial as inventories form a substantial part of the primary business engagement.

The aim of this study was to investigate the Impact of inventory management on financial performance of listed manufacturing firms in Sri Lanka. Studies conducted in Sri Lanka has mainly tested the effect of inventory management by taking profitability ratios as proxy for financial performance. However, this study add value to context by investigating the impact beyond the dimension of profitability. This study investigated the impact of inventory management on financial performance in the dimensions of profitability, cash flows and market value of firm.

According to that, the independent variables used in the study are inventory conversion period and inventory turnover which are proxies for inventory management. This study also used control variables which were derived through past literatures. These variables were used to give a strong understanding and influence of independent variables to the results generated and to provide realistic results. The control variables used in the study are operating efficiency, firm’s growth and firm’s size. Moreover, the dependent variables used in the study are return on assets, cash flow from operations, market value added of a firm. These are used as proxies for financial performance in dimensions of profitability, cash flows and market value of a firm. Afterward, data was collected for this research using secondary data using published annual reports for 5 years. The sampling technique for sector selection was judgmental sampling technique. All listed manufacturing companies were taken as the sample amounting to 29 companies. Panel data regression analysis was performed to analyse the collected data. Data were analysed in the form of descriptive analysis, correlational analysis and Regression analysis.

The results of the study were that inventory conversion period has a significant negative relationship with all return on assets, cash flow from operations and market value added of a firm while inventory turnover is insignificantly related to all return on assets, cash flow from operations and market value added of a firm. Among control variables used in the study, firm’s size has a significant positive impact to all return on assets, cash flow from operations and market value added of a firm. Therefore, this study concluded that inventory conversion period has a significant negative impact to financial performance of a firm and inventory turnover is insignificantly related to financial performance of a firm.

This study provides further understanding on the impact of inventory management on financial performance of listed manufacturing companies in Sri Lanka. This study will be an important indicator to firms on the graveness of managing their inventories. This study recommends managers of a firm to reduce the time taken to convert inventories into sales. By doing so they are able to increase their profitability, cash flows and market value of the firm since lower the days taken to convert inventories to sales, higher the financial performance vice versa.

This study also recommend that managers of a firm should take steps in increasing the size of their firms as results indicates that firm’s size has a positive effect on financial performance of a company. Where larger the size of a firm higher the performance vice versa.

Mwangi, W. and M.T. Nyambura. “The Role of Inventory Management on Performance of Food Processing Companies: A Case Study of Crown Foods Limited Kenya.” European Journal of Business and Social Science, 2015.

Shardeo, V. “Impact of Inventory Management on the Financial Performance of the Firm.” IOSR Journal of Business and Management, 2015.

Golas, Z., and A. Bieniasz. “Empirical Analysis of the Influence of Inventory Management on Financial Performance in the Food Industry in Poland.” Inzinerine Ekonomika-Engineering Economics, 2016.

Karim, N. et al. “Inventory Management Effectiveness of a Manufacturing Company – Malaysian Evidence.” International Journal of Law and Management, 2018.

Anshur, A.S. et al. “The Role of Inventory Management on Financial Performance in Some Selected Manufacturing Companies in Mogadishu.” International Journal of Accounting Research, 2018.

Trujillo, P. “Times Horrific Inventory Control Almost Killed These Companies.” 2016.

Akindipe, O. “Inventory Management – A Tool for Optimal Use of Resources and Overall Efficiency in Manufacturing SMEs.” Journal of Entrepreneurship Management and Innovation (JEMI), vol. 10, no. 4, 2014.

Lwiki, T. et al. “The Impact of Inventory Management Practices on Financial Performance of Sugar Manufacturing Firms in Kenya.” International Journal of Business, Humanities and Technology, 2013.

Stanger, S.H. et al. “What Drives Perishable Inventory Management Performance? Lessons Learnt from the UK Blood Supply Chain.” Supply Chain Management: An International Journal, 2012.

Kontus, E. “Management of Inventory in a Company.” 2014.

Roumiantsev, S. and S. Netessine. “Inventory and Its Relationship with Profitability: Evidence for an International Sample of Countries.” 2007.

Leachman, C. et al. “Manufacturing Performance: Evaluation and Determinants.” International Journal of Operations & Production Management, vol. 25, no. 9, 2005, pp. 851–874.

Shah, R. and H. Shin. “Relationship among Information Technology, Inventory and Profitability: An Investigation of Level Invariance Using Sector Level Data.” Journal of Operations Management, 2007.

Mathuva, D.M. “The Influence of Working Capital Management Components on Corporate Profitability: A Survey of Kenyan Listed Firms.” Research Journal of Business Management, 2010.

Augustine, A. and O. Agu. “Effect of Inventory Management on Organisational Effectiveness.” Information and Knowledge Management, 2013.

Shin, S. et al. “Effect of Inventory Management Efficiency on Profitability: Current Evidence from the U.S. Manufacturing Industry.” Journal of Economics and Economic Education Research, 2015.

Folinas, D. and C.Y. Shen. “Exploring Links among Inventory and Financial Performance in the Agricultural Machinery Industry.” International Journal of Food and Agricultural Economics, 2014.

Altan, M. and G. Sekeroglu. “The Relationship between Inventory Management and Profitability: A Comparative Research on Turkish Firms Operated in Weaving Industry, Eatables Industry, Wholesale and Retail Industry.” International Journal of Mechanical and Industrial Engineering, 2014.

Sunday, O. and E. Joseph. “Inventory Management and SMEs Profitability: A Study of Furniture Manufacturing, Wholesale and Eatery Industry in Delta State, Nigeria.” Journal of Finance and Accounting, 2017.

Sitienei, E. and F. Memba. “The Effect of Inventory Management on Profitability of Cement Manufacturing Companies in Kenya: A Case Study of Listed Cement Manufacturing Companies in Kenya.” International Journal of Management and Commerce Innovations, 2015.

Gaur, V. and S. Kesavan. “The Effects of Firm Size and Sales Growth Rate on Inventory Turnover Performance in the U.S. Retail Sector.” Retail Supply Chain Management, 2008.