+91 6002993949

submission@iarconsortium.org

Open Access

ISSN (Print) : 2708-5139

ISSN (Online) : 2708-5147

The 2020 World Economic forum at Davos was significant in a way that climate change and sustainability accounting became the dominating agenda for the gathering. It was quite evident that the concern on climate, which laterally touched the corporate in the past, has now become mainstream. The most important issue for everyone to understand a business is accounting and in the contemporary days of global accounting, reporting on non-finance areas is the key reporting towards accountability of an enterprise. Public sectors are accountable not merely to shareholders but to the stakeholders as well. Accounting on sustainability enables organizations to communicate to the stakeholders its goals and to ascertain what they are pursuing to accomplish. It is the businesses connect to the society. Thereby scope of accounting is widened to include financial details and also non-financial details. Traditionally in the preparation of Financial statements of a corporate included Income and Expenses reflected in profit and loss statement, Assets, Equity and Liabilities shown in Balance sheet and Cash flow statement. In this paper HPCL has been considered and the authors reveal that HPCL is transparent and consistent, when it comes to sustainability reporting. It is very imperative that Sustainable accounting is not a regulatory or statutory obligation but a social commitment of the corporate towards the country and consumes the resources therefore it is largely dependent on the commitment levels of the corporate. Sustainable accounting involves Integrated thinking, reporting and sustainability. Sustainability accounting goes beyond disclosures.

The term Accounting refers to the summary, analysis and reporting of financial transactions relating to business. It reflects the reliability on the financial soundness of company. Corporate annual reports no longer focus solely on the accounts providing quantitive information about business transactions but volunteer providing qualitative information to the stakeholders. The American Institute of Certified Public Accountant defined the term Accounting as “Accounting is the art of recording, classifying and summarising in significant manner and in terms of money, transactions and events which are, in part, at least of a financial character and interpreting the results thereof.”

The need for sustainable reporting is gaining relevance because of utility of users of financial statements to understand non finance dimensions of the business. As a result of change in business environment and competition need for sustainable accounting has become inseparable part of financial statements and reporting.

In this paper sustainability performance of HPCL selected indicators for Economic, Social and Environment by taking into factors Total Revenue, Net Profit, Contribution to exchequer, crude oil processing and sales volume under economic factors, Social factors include Safe man hours, New LPG connections, CSR expenditure and projects Akshyapatra, Nanhi Kali, Unnati. The measurement of Environment includes factors say Energy conservation at refineries, generation of wind energy, solar power capacity and ethanol blending.ng and reporting allows companies to present qualitative as well as quantitative data about the moment of the environment, social and human capital and the priorities of corporate governance.

The 2020 World Economic forum at Davos was significant in a way that climate change and sustainability accounting became the dominating agenda for the gathering. It was quite evident that the concern on climate, which tangentially touched the corporate in the past, has now become mainstream. The most important issue for everyone to understand a business is accounting and in the contemporary days of global accounting, reporting on non-finance areas is the key reporting towards accountability of an enterprise. Sustainability accounting has gradually translated into business risk, calling for a significant reshaping of finance creating sustainability impact and ensuring better risk adjusted returns to investors is destined to become the key agenda for the top management of any company in any country.

The relevance of sustainability accounting and reporting is gaining importance globally because of stakeholders expectations from annual reporting is going beyond financial statements. It was for a good period of time corporates are of the view the manner of reporting, since shareholders may not be able to understand and analyze Annual report if all the information is provided in it. This opinion is soon becoming a myth.

The contribution of the Brundtland report, The World Commission on Environment and Development provided scope and clarity of the term sustainability development by providing landmark definition as a development that meets the needs of the present without compromising the capability of upcoming generation to meet their own needs. This definition provided need to realize for corporates to understand the term finance as transformation including sustainable accounting. Sustainability accounting enables the systematic identification and interlinking of the social, environmental and economic costs and benefits of organizational strategies and actions and embeds these considerations into organizational decision making [1]. The present literature illustrates that public sector companies implemented sustainable accounting and reporting practices. The research emphases to the present date have addressed sustainability reporting practices [2,3], Guthrie and Farneti, in order to disclose information not limited to the information already included in financial accounting and provide this information and disclose standards to stakeholders, various institutions have developed “guidelines” for Sustainability Reporting (SR), the preeminent reports being those produced by the Global Reporting Initiative (GRI). Goswami and Lodhia, add that sustainable reporting is an important means for assessing an organization's performance in relation to economic, social and environmental issues. Within the public sector, sustainable reporting and accounting are essential for enabling citizens to judge the extent to which a respective level of government provides social welfare. The drivers of sustainability reporting [4,5] environmental management accounting [6] and relevance of stakeholder engagement than shareholder [7]. Grey et al. highlights that the public sector is potentially enormous with the size of capital and investment and exceptionally diverse, consequently making its social and environmental accounting and accountability too important to be ignored; especially considering that 50% of a country’s economic activity and employees go through these organizations in order to promote sustainability. However, sustainability reports are taking place more slowly than those of other sectors [8,9] and there is little research related to social and environmental accounting, accountability and sustainability in the public sector.

Therefore, observing earlier studies there was a significant lack of research regarding studies on the publication of sustainable accounting and reporting in public sector exclusively petroleum sector.

In order to make promote transparency and accountability by the corporates the contribution of the theories of Accounting need to be highlighted namely Agency theory, Signaling theory, Theory of Legitimacy and Stakeholders theory advocate enhancing the trust of shareholders by enhancing transparency of corporate reporting by providing sustainable dimensions of business. The corporates more so public sector companies involving their business transactions with the nature must adopt sustainable accounting as a part of accounting to ensure the principle of transparency and disclosure of their environmental, social and economic activities. The sustainable accounting dimensions of corporate reporting include aspects of Sustainability, Flexibility and Vulnerability Sustainability includes the impact of the level of debt on Public Sector Company. Flexibility refers to the cash flows produced i.e., EBITDA or PBIDT / operating ratio and Vulnerability refers to the ratio of own revenues to that of grants.

Hindustan Petroleum Corporation Limited (HPCL) is one of the largest public sectors Petroleum and Natural Gas Company and Government of India enterprises listed on BSE and NSE Exchange. HPCL is a Global Fortune 500 (ranked 327) company conferred with a Navratna Status and a Forbes 2000 (ranked 1302) Company. The company has identified the need to report sustainability separately from Annul Report from the financial year 2014-15. The report discloses HPCL’s performance on environmental, social and economic parameters. The report is based on the Global Reporting Initiative’s (GRI) G4 Guidelines in accordance to the “Core” criteria for reporting, along with disclosures under Oil and Gas Sector Supplement (OGSS).

The success of sustainability accounting and reporting is largely dependent accountability and transparency that being the challenge today.

Sustainability Performance

To understand the relevance of sustainability performance of HPCL, indicators are classified broadly into Economic, Social and Environment. The factors of measurement of above said indicators include financial and physical performance. To fathom the Economic aspects of HPCL, selected items are Total revenue, Net Profit and Contribution to the Exchequer measured in ₹ Crore and Crude oil processing and Sales volume measured in Million Metric Tonnes (MMT) (Table 1).

Table 1: Economic Analysis of HPCL from 2013-2020

| Year | Total Revenue ₹ Crore | Net Profit ₹ Crore | Contribution to Exchequer ₹ Crore | Crude oil processing MMT | Sales Volume MMT |

| 2013-14 | 2,24,333 | 1,734 | 36,423 | 15.51 | 30.96 |

| 2014-15 | 2,08,332 | 2,733 | 40,752 | 16.18 | 31.95 |

| 2015-16 | 1,98,888 | 3,726 | 52,235 | 17.23 | 34.21 |

| 2016-17 | 2,15,318 | 6,209 | 65,674 | 17.81 | 35.23 |

| 2017-18 | 2,45,935 | 6,357 | 69,752 | 18.28 | 36.87 |

| 2018-19 | 2,98,564 | 6,029 | 73,350 | 18.44 | 38.71 |

| 2019-20 | 2,89,255 | 2,637 | 76,133 | 17.18 | 39.64 |

The term Total Revenue include Revenue from operations i.e., Gross sale of products, other operating revenues and other income. During study period 2013-14 to 2015-16 the business environment of the petroleum industry experienced complex and challenging situations since the Indian economy witnessed a growth rate of less than 5% along with a depreciating rupee. From the financial years 2016-17 to end 2018-19 period revenues of the company has been improving sustainably. Last quarter of Financial Year 2019-20, worldwide experienced exceptional events like outbreak of COVID-19 pandemic leading to global and nationwide lock downs and impacting demand contraction on the back of sluggish global economic activities. This, combined with the inability of oil producing countries to reach a consensus to rebalance the supply demand situation, led to unforeseen volatility in crude oil and product prices. Financial year 2020 experienced steepest falls in crude oil prices seen in the last two decades due to excess inventories, lower demand, geopolitical situations. The nationwide lock down to contain the spread of the pandemic in India led to substantial demand contraction in the very last part of March 2020.

The Net profit i.e., Profit after Tax (PAT) during the study period has shown fluctuating trend. The company’s long term business strategy was focused on investing in new infrastructure in its core business areas of refining and marketing and also company focused on finding out new avenues to move up the value chain and also meeting the requirements of the country (Figure 1).

Figure 1: Economic Analysis of HPCL from 2013-2020

The Company during the study period has shown achieving milestones year on year across all facets of the business. During the last three consecutive years i.e., 2016-17 to 2018-19, company has shown an excellence and sustainable performance achieving profit after tax exceeding ₹ 6000 crore. The company in the financial year 2017-18 reported highest ever profit after tax of ₹ 6,357 Crore. We can observe Financial year 2019-20 is an exceptional year wherein the company reported lowest Net profit compared to previous years 2013-14 to 2018-19 due to the factors discussed above.

The prices of petrol and diesel have been market determined by the Government of India with effect from June 26, 2010 and September 19, 2014. Since then the pricing of petrol and diesel are decided in line with international product prices. The contribution to central exchequer and State exchequer in the 2018-19 ₹3,65,113 crore and ₹2,30,325 crore respectively. During the Financial year 2018-19 the total contribution of petroleum sector to exchequer ₹ 5,95,438 crore. During the financial year 2019-20 though economy was affected by Covid but still petroleum sector total contribution to the exchequer stood at ₹ 5,55,370 crore, while the contribution to central exchequer and State exchequer in the 2019-20 ₹3,34,315 crore and ₹2,21,056 crore, respectively. The contribution to exchequer includes Tax/Duties on Crude oil & Petroleum products and Dividend to Government/Income tax etc. The company during the study period has shown increasing in trend indicating increase excise duty, corporate tax, dividend tax, sales tax and service tax.

The analysis of Crude oil processing and Sales volume of the company during the financial year 2013-14 has shown to record robust physical sales growth by implementing effective marketing strategies under challenging business environment. HPCL refineries processed 15.51 MMT of crude, achieving 105% capacity utilization. In 2013-14, the company registered total product sale of 30.96 MMT (including exports) viz-a viz 30.32 MMT during the preceding year. The corporation further improved its market share by 0.71% to 20.90% in 2013-14.

During the year 2014-15 company’s refineries at Mumbai and Visakh higher crude processing, resulted in achieving a combined refining thruput of 16.18 million tonnes with a capacity utilisation of 109%. The refineries also achieved a highest ever combined distillate yield of 77.5%, by improving the yields of value-added products. During financial year 2015-16, refineries achieved a combined refining throughput of 17.23 MMT, with a capacity utilisation of 116%, which is the highest ever achieved by the refineries. Higher crude processing by refineries has translated into best ever production of petroleum products. During 2015-16, the company has achieved the highest-ever sales volume of 34.21 MMT (including exports), with a market share of 21.25%, maintaining a growth rate above industry. The financial year 2016-17 has witnessed optimization of the crude basket by adding three new types of crude oil that will enable larger savings in the future.

During these fiscal refineries have surpassed their combined crude processing record by achieving a combined refining throughput of 17.8 MMT and a capacity utilization of 113% against the previous throughput of 17.2 MMT in 2015-16. Moreover, both Mumbai and Visakh refineries registered MOU ‘Excellent’ rating for the ninth year in succession. The sales volumes this year were recorded at 35.23 MMT. Domestic sales grew by 2.5% over the last year to reach a market share of about 21% among the public-sector oil companies. During 2017-18 fiscal, the company achieved all-time high combined refining throughput of 18.28 Million Metric Tonnes (MMT) surpassing the previous best of 17.81 MMT achieved in 2016-17. Mumbai and Visakha refineries recorded highest ever production numbers across product offerings. Crossed a milestone of 36 MMT and achieved sales of 36.87 MMT (including exports) and marketing sales 36.25 MMT with a growth of 4.4%. The company has achieved the highest ever monthly sales of 3.44 MMT in March 2018. The crude processing and sales volume have improved further during 2018-19 and achieved 18.44 MMT and 38.71 MMT respectively. refineries have been consistently performing over the years, maintaining a stellar track-record. During 2019-20, the company with effective management of intermediate streams evacuation as well as meticulous handling of two grades of MS and HSD during the interim period of rollout of BS-VI grade of fuels at Mumbai and Visakhapatnam refineries and a key factor in achieving the performance of 8.07 MMT and 9.11 MMT refineries at Mumbai and Visakhapatnam sustained sound physical performance.

The company with its constant focus on customer satisfaction despite stiff competition and other economic challenges during the financial year 2019-20 achieved a landmark in sales volume of 39.64 MMT (including exports) with a market share of around 21% amongst the PSU categories (Table 2).

Table 2: Social Impact Assessment of HPCL

| Year | Safe Man- Hours (Million) | PMUY programme New LPG Connections (Million) | Expenditure on CSR Activities (₹ Crore) | Project Akshayapatra Number of children provided with mid-day Meals | Project Nanhi Kali Number of Girl children supported in backward areas | Project Unnati Students trained with basic computer education |

| 2013-14 | 12.44 | NA | 23.74 | 5,000 | 7,552 | 4,100 |

| 2014-15 | **** | NA | 34.07 | 5,000 | 10,052 | 4,100 |

| 2015-16 | 15.00 | NA | 71.67 | 12,000 | 11,000 | 5,000 |

| 2016-17 | 18.34 | 5.30 | 108.11 | 12,585 | 12,000 | 8,000 |

| 2017-18 | 21.54 | 4.20 | 156.86 | 15,000 | 13,000 | 8.000 |

| 2018-19 | 24.59 | 10.10 | 159.81 | 15,000 | 13,000 | 12,000 |

| 2019-20 | 27.52 | 19.56 | 182.24 | 20,000 | 13,000 | 12,000 |

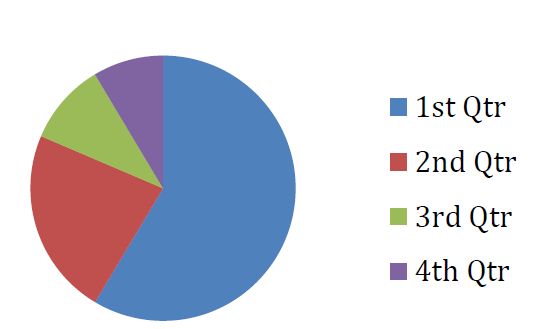

During the stpudy period it is observed that one of the key factors for consistent outstanding performance of the company is work force and importance attributed as a corporate culture. The company has given at most importance to their safety and working towards ‘zero incident’. All the employees and contract staff are imparted comprehensive training on health and safety. A host of technical and behavioral programmes including unique initiatives “Suraksha Parishad” and “Safety on Wheels” for effective capability building and sensitization for enhanced occupational and road safety has been taken up. To ensure emergency preparedness, mock drills are regularly conducted to keep everyone in a state of readiness. During the selected period because of aforesaid measures the company achieved year on year milestones in safety, saving 15 million man-hours during 2015-16 to 27.52 million man-hours of safe operations during the financial year 2019-20 (Figure 2).

Figure 2: Social Impact Assessment of HPCL from 2013–14 to 2019–20 across Key CSR Initiatives

It is an important moment to study contribution of HPCL to various socioeconomic development programmes selected for the study initiated by Government of India (Figure 3).

Pradhan Mantri Ujjwala Yojana is an ambitious social welfare scheme of Government of India launched on 1st May 2016. The PMUY programme is aimed to provide LPG connections to BPL households in the country.

Figure 3: Expenditure on CSR Activities from 2013–14 to 2019–20

The scheme is aimed at replacing the unclean cooking fuels mostly used in the rural India with the clean and more efficient Liquefied Petroleum Gas (LPG) (Figure 4).

Since initiative taken by Government of India, Company has been very effective in meeting the programme goals. During 2016-17, 5.30 million new LPG connections were given and during the year 2018-19 number of new LPG connections were nearly doubled i.e., 10.10 million. The company during the year 2019-20 provided clean cooking fuel solution to poor households, especially in rural areas. HPCL along with other PSU OMCs achieved the target of 8 Crore PMUY connections in September 2019 way forward of the target date of March 31, 2020. A total of 2.15 Crore PMUY LPG connections were provided.

Project Akshayapatra program is implemented during the year 2011-12 and aimed to provide nutritional mid-day meals to children going to government schools to prevent drop out, to increase the attendance and to tackle the malnutrition among them, thereby contributing to eradication of extreme poverty and hunger, achieving Universal Education, promoting Gender equality and empowering women.

Under this programme, during the years 2013-14 and 2014-15 direct access to food for the under privileged children by providing mid-day meals in Visakhapatnam and Guwahati for 5000 children and providing Food distribution vehicles & vessels at Medak District in Andhra Pradesh through Akshaya Patra, who work in partnership with various State Governments of India. This wholesome meal is often the only nutrition the students have during the day. The food lab therefore strives to ensure that the meals are appealing to children, while also meeting the requirements of a growing child. The Foundation’s centralized kitchens, among the largest in the world, use innovative technology to cook hundreds of thousands of meals in a few short hours. The decentralized kitchens reach out to children in the remotest areas of India while also creating employment for hundreds of women. The number of children provided with mid-day meals during the study period 2013-14 to 2019-20 has shown a substantial increase in percentage terms as well as in numbers.

Project Nanhi Kali is an exclusive project for girl child. This programme aimed to up bring girl child to attend school and not restricting to the domestic chores.

Figure 4: New Gas Connections under PMUY from 2013–2020

Most of the families benefitted are daily wage laborers, vegetable vendors, rickshaw pullers and other economically backward groups. The number of Girl children supported in backward areas during the study period 2013-14 to 2018-19 has shown significant increase. During the financial years 2017-20 the education of 13,000 girl children are provided under this programme.

Project Unnati is a programme aimed at training students in the basic computer education. The company has provided good number of students covered during the study period. During the year 2013-14, 4,100 students were benefited and in the years 2018-19 and 2019-20 touched 12,000 students. Overall, during the study period, the contribution to the society under this programme has shown an increasing trend.

The company has proven with above discussion and analysis its readiness and always geared to contribute towards nation building by effectively implementing various initiated (Table 3).

Table 3: HPCL Environmental Impact Assessment

| Year | Energy Conservation at Refineries (SRFT) | Solar power capacity | Wind energy generation (kWh) | Pipeline (MMT) | Ethanol Blending (%) |

| 2013-14 | 25,535 | ------ | 560 L | 15.69 | --- |

| 2014-15 | 18,832 | 2.00 L kWh | 544 L | 14.91 | --- |

| 2015-16 | 19,170 | 3.35 L kWh | 447 L | 17.61 | 3.30 |

| 2016-17 | 35,500 | 3.80 L kWh | 9.62 Crore | 17.91 | 3.51 |

| 2017-18 | 18,608 | 12.00 L kWh | 16.95 Crore | 20.40 | 2.11 |

| 2018-19 | 30,710 | 22.60MWp | 19 Crore | 21.50 | 5.50 |

| 2019-20 | 25,586 | 32.50 MWp | 18.6 Crore | 21.20 | 4.96 |

HPCL ever since its inception has been proven responsible corporate citizen. Year 2013-14 is the year of completion of 40 years of existence. During the selected study period 2013-19, it is found that company was very keen towards conservation of energy and for attaining sustainability, concentrated on the improving productivity, efficiency and reduction in emissions by identifying areas for substantial savings in both refineries namely Mumbai and Visakhapatnam, thereby resulting in savings of 25,535 standard refinery fuel tonnage per year and in monetary terms approximately ₹106 crore. It is observed the component energy for the company is one of the most critical aspects of operation of refineries therefore given highest priority for operating cost and conserving energy. During study period SRFT has shown fluctuating trend but achieved highest 30,710 proving operational excellence. Year 2019-20 being a year of exceptional events the company has reported a decline in SRFT compared to previous year (Figure 5).

Figure 5: Various Forms of Energy Generation from 2013 to 2020

The above chart, sunburn chart depicts various forms of energy generation renewable and nonrenewable sources by HPCL over a period of seven years. These seven years being the most happening years from the sustainability perspective in India.

The company has shown strong overall performance and productivity not only at its refineries but across the entire supply network of product pipelines, depots, terminals and LPG bottling plants. It has been found that during the period of study HPCL was making every year record and recorded the pipeline throughout 21.50MMTPA during 2018-19 and 21.20MMTPA during financial year 2019-20. 2014-15 is a year Visakhapatnam refinery has been shut down as a precautionary measure due to cyclone HUDHUD (12th October 2014) that hit east coast of India, thereby pipeline 14.91MMT. The initiative of pipeline throughout made the company in minimizing costs involved in logistics and reducing carbon footprint.

The Government of India has mandated Ethanol blending in motor spirit towards marching the country towards energy security by reducing dependency on imported crude and conserving foreign currency reserves. The company has given equal importance towards achieving balancing stakeholders’ returns and shareholders returns. The company is actively involved in Ethanol blending programme to reduce carbon intensity especially transportation sector. During the year 2013-14, company procured 98,844 KL of ethanol and remaining period of study shown consistent increase and in the years 2017-18 and 2018-19 recorded 2.11 percent and 5.50 percent of ethanol blending. During the year 2019-20 Ethanol-blending in petrol has reported 4.96 percent. The Government of India to give encouragement to agricultural sector aiming to achieve 10 percent EBP by 2022.

HPCL has been studied in-depth and the authors confide that HPCL is transparent and consistent when it comes to sustainability reporting. HPCL is a proven Good Samaritan among the corporate players in India. The various practices of the company not only lead path to achieve sustainability goals but also sustainable value creation and there by mitigating business risk.

It is high time for the corporates to look beyond the numbers of the financial statements and focus on sustainability of the enterprise. The key point that authors have been stressing upon is that the sustainability accounting has to be finalized and reporting of the same be made mandatory has seen the light with Ministry of Corporate Affairs is in the process of issuing a guideline, making the corporate sustainability reporting a mandatory item in the annual reports in the years to come.

Hopwood, A. et al. Accounting for Sustainability: Practical Insights. London: Earthscan, 2010.

Adams, C. et al. “Measurement of Sustainability Performance in the Public Sector.” Sustainability Accounting, Management and Policy Journal, vol. 5, no. 1, 2014, pp. 46–67.

Ball, A. et al. Sustainability Accounting and Accountability in the Public Sector. Sustainability Accounting and Accountability. Oxon and New York: Routledge, 2014.

Farneti, F. and B. Siboni. “An analysis of the Italian governmental guidelines and of the local governments’ practices for social reports.” Sustainability Accounting, Management and Policy Journal, vol. 2, no. 1, 2011, pp. 101–125.

Global Reporting Initiative (GRI). Sustainability Reporting Guidelines: Data Legend. Amsterdam: Global Reporting Initiative, 2013.

Rolland, D. and J. O’Keefe Bazzoni. “Greening corporate identity: CSR online corporate identity reporting.” Corporate Communications: An International Journal, vol. 14, no. 3, 2009, pp. 249–263. https://doi.org/10.1108/13563280910980041.

Yadava, R. and B. Sinha. “Scoring sustainability reports using GRI 2011 guidelines for assessing environmental, economic and social dimensions of leading public and private Indian companies.” Journal of Buasiness Ethics, vol. 138, no. 3, 2016, pp. 549–558. https://doi.org/10.1007/s10551-015-2597-1.

Domingues, A. et al. “Sustainability reporting in public sector undertakings: exploring the relation between the reporting process and organizational change management.” Journal of Environmental Management, vol. 192, 2017, pp. 292–301.

Greiling, D. et al. “Sustainability reporting in the Austrian, German and Swiss public sector.” International Journal of Public Sector Management, vol. 28, no. 4–5, 2015, pp. 404–428.